Markets

Massive Bailout’ Needed in China, Banking Analyst Chu Says

Charlene Chu, a banking analyst who made her name warning of the risks from China’s credit binge, said a bailout in the trillions of dollars is needed to tackle the bad-debt burden dragging down the nation’s economy.

Speaking eight days after a Communist Party newspaper highlighted dangers from the build-up of debt, Chu, a partner at Autonomous Research, said she was yet to be convinced the government is serious about deleveraging and eliminating industry overcapacity.

She also argued that lenders’ off-balance-sheet portfolios of wealth-management products are the biggest immediate threat to the nation’s financial system, with similarities to Western bank exposures in 2008 that helped to trigger a global meltdown.

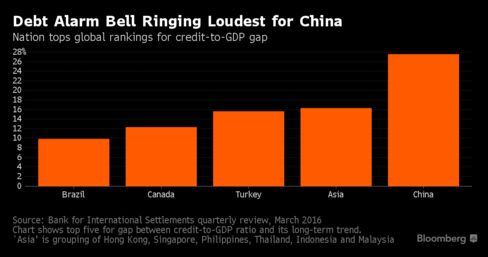

The former Fitch Ratings analyst uses a top-down approach to calculating China’s bad-debt levels as the credit to gross domestic product ratio worsens, requiring more credit to generate each unit of GDP.

While Chu is on the bearish side of the debate about the outlook for China, she’s not alone. In a report on Monday, Societe Generale SA analysts said that Chinese banks may ultimately face 8 trillion yuan ($1.2 trillion) in losses and a bailout from the government, citing the scale of soured credit within state-owned enterprises.

Interviewed in Hong Kong last week, Chu estimated as much as 22 percent of all China’s outstanding credit may be nonperforming by the end of this year, compared with an official bad-loan number for banks in March of 1.75 percent.

Question

What do you see as the biggest risk in the financial system?

Answer

“China’s debt problems are large and severe, but in some respects a slow burn. Over the near term, we think the biggest risk is banks’ WMP portfolios. The stock of Chinese banks’ off-balance-sheet WMPs grew 73 percent last year. There is nothing in the Chinese economy that supports a 73 percent growth rate of anything at the moment. Regardless of all of the headlines and announcements about the authorities cracking down on WMPs, they have done very little, really, and issuance continues to accelerate.

“We call off-balance-sheet WMPs a hidden second balance sheet because that’s really what it is — it’s a hidden pool of liabilities and assets. In this way, it’s similar to the Special Investment Vehicles and conduits that the Western banks had in 2008, which nobody paid attention to until everything fell apart and they had to be incorporated on-balance-sheet.

“The mid-tier lenders is where these second balance sheets are very large. China Merchants Bank is a good example. Their second balance sheet is close to 40 percent of their on-balance-sheet liabilities. Enormous.”

Question

Who buys a WMP?

Answer

“The products used to be predominantly sold to the public, but now they’re increasingly being sold to banks and other WMPs. We’re starting to see layers of liabilities built upon the same underlying assets, much like we did with subprime asset-backed securities, collateralized debt obligations, and CDOs-squared in the U.S. The range of assets is much more diverse than mortgages, but we have significantly less visibility on the assets than we did with subprime.”

Question

After the People’s Daily commentary, is it clear that the government is serious about deleveraging?

Answer

“The word deleveraging should not be used when discussing China. Deleveraging means negative credit growth, or a contraction in the ratio of credit to GDP. China is nowhere close to deleveraging. Over the years, I have learned from watching the authorities respond to issues like WMPs that there is often a large divergence between official rhetoric and actual action. It’s encouraging to see policy makers acknowledge the severe overcapacity problem, but I am sceptical that much headway will be made any time soon, given how painful implementation will be and the pushback they will inevitably receive at local levels.”

Question

Is a financial crisis or a very dramatic economic slowdown now inevitable?

Answer

“Not yet, but we’re getting there because the problem is getting so big. We’re still adding 10 to 20 percentage points to the ratio of credit to GDP every year — that has not changed despite the fact that credit growth has decelerated. If the government was to come out with a very aggressive — and it would have to be incredibly aggressive — bailout package for corporates, as well as financial institutions, it would do a lot in terms of dealing with some of this debt overhang and getting rid of the black cloud that’s hanging over the country. However, the idea that China needs a massive bailout in the trillions of U.S. dollars isn’t something I think the authorities are on board with or accept yet. They still believe they can grow out of it.”

Question

Could your assessment of China’s debt situation be based on faulty assumptions?

Answer

“If we’re wrong, and there’s always a chance of that, it’s going to be because we’re under-appreciating the economic growth potential in China — that there is some more strength to the consumption story and services story than we sense now, and that these are about to take off and propel the country out of these debt problems.”

Question

How does China’s debt build-up compare to Japan’s previously?

Answer

“If you look at Japan, the credit expansion wasn’t anywhere close to the size of China’s, and China’s continues to grow at a rapid rate. There is also a somewhat Wild West, chaotic nature to a lot of the shadow banking going on in China that is different from the shadow credit we saw in Japan. What’s positive for China is that they’ve got a leadership team that is not as afraid as the Japanese leadership is of radical change. So, if China’s authorities ever do decide debt is the center of their problems and they need to do something about it, we won’t have decades of complacency with nothing really done. On the negative side, China has a much weaker social safety net and a much poorer population, which makes social and political instability a real concern.”

Question

What’s your assessment of China’s capital flows?

Answer

“The party line is that outflows are all about offshore debt repayment, but that accounts for a minority of the flows we are seeing. We think most of the money is leaving through trade mis-invoicing, which is very hard to shut down. Although capital outflows have quieted down, the underlying motivations for people to move their money out of the country are still there. This problem has not gone away.”