Markets

Emerging Markets Slide as Dollar Strengthens

Financial markets are reawakening to the risk that the U.S. expedites interest-rate increases, and that’s buoying the dollar while denting emerging markets and commodities.

The dollar climbed to a seven-week high and Treasuries fell, pushing two-year yields to highest since April, after Atlanta Federal Reserve President Dennis Lockhart and San Francisco’s John Williams said Tuesday two rate hikes may be warranted this year. Chinese stocks tumbled to a two-month low, while the rand led the selloff versus the greenback amid mounting political tension in South Africa. Copper and gold fell for the first time in four days.

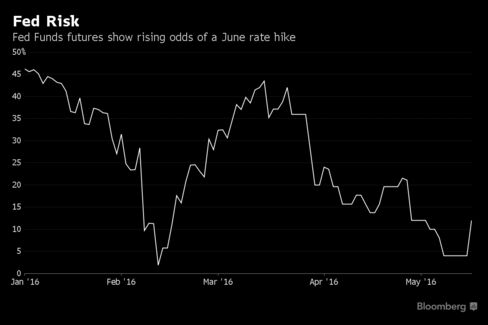

The dollar has rebounded in May after declining in the previous three months as the Fed pushed back expectations for rate increases this year. A strengthening U.S. economy and the biggest jump in consumer prices in three years have led traders to boost the odds of a move in June threefold to 12 percent. The Fed will release the minutes of its April policy meeting on Wednesday.

Currencies

The Bloomberg Dollar Spot Index advanced 0.4 percent at 6:04 a.m in New York. Australia’s dollar lost 0.8 percent. The yen slipped 0.3 percent to 109.43 per dollar, after earlier strengthening as much as 0.4 percent. The euro weakened 0.4 percent to $1.1268.

The MSCI Emerging Markets Currency Index fell 0.5 percent, the most in two weeks. South Korea’s won, Russia’s ruble, the Mexican peso and Malaysian ringgit dropped at least 0.8 percent.

Stocks

The Stoxx Europe 600 Index slipped 0.1 percent. Burberry Group Plc dropped 3.7 percent after the luxury-goods retailer added to the industry’s gloom by posting a second straight drop in annual earnings. Sonova Holding AG tumbled 7.1 percent after the Swiss hearing-aid maker’s second-half earnings missed estimates.

Futures on the S&P 500 were little changed after equities tumbled on Tuesday. Investors will look Wednesday to earnings from retailers including Target Corp., Staples Inc., Lowe’s Cos. and Urban Outfitters Inc. for further indications on the health of U.S. consumers after a slew of disappointing results cast doubt on their willingness to spend.

Minutes from the Fed’s April meeting will also be in focus for clues on the trajectory of interest rates after hawkish comments from regional presidents. The first month with even odds of higher borrowing costs also moved up to November from December.

The MSCI Asia Pacific Index lost 0.8 percent, led by declines in consumer-goods producers. Suzuki Motor Corp. plunged 9.4 percent in Tokyo after saying it used an improper method to test the fuel efficiency of its vehicles.

Chinese stock led declines in emerging markets, with the Hang Seng China Enterprises Index of mainland companies listed in Hong Kong losing 1.5 percent.

Commodities

Copper fell along with other metals amid rising supplies and an uncertain demand outlook in China, the world’s top consumer. Antofagasta Plc, a Chilean copper producer, said it isn’t counting on an improving global economy and expects low copper prices for another year or two, according to a statement from Chairman Jean-Paul Luksic.

Copper for delivery in three months slid 1.5 percent. Gold for immediate delivery lost 0.5 percent.

Oil fell 0.3 percent to $48.16 a barrel in New York after closing on Tuesday at the highest since Oct. 9. Government data Wednesday is forecast to show supplies slid for a second week.

Bonds

The yield on U.S. two-year Treasuries climbed to 0.84 percent, the most since April 27. The 10-year yield was little changed at 1.77 percent. That compares with a one-month low of 1.70 percent at the end of last week. Similar-maturity debt in Singapore declined by the most in three weeks, lifting the yield by five basis points to 2.01 percent.

Jan Hatzius, the chief economist at Goldman Sachs Group Inc., warned that bond investors aren’t prepared for the Fed to raise interest rates despite officials having flagged the possibility of such a move.

“The market’s underestimating their willingness to follow through on what they say,” Hatzius said in an interview on Bloomberg Television. “If you look at where the yield curve is priced — how little normalization of monetary policy is discounted — that’s very striking.”

Heta Asset Resolution AG bonds jumped after creditors reached an agreement with the Austrian government to settle a dispute over 11 billion euros ($12.4 billion) of guaranteed debt. The 1.25 billion euros of 4.25 percent notes due Oct. 31 climbed about five cents on the euro to 88 cents, according to data compiled by Bloomberg.