The Central Bank of Nigeria-led Monetary Policy Committee (MPC) left the interest rate unchanged at 11.5 percent on Tuesday despite the devaluation of the Nigerian Naira to N410.25 (adoption of NAFEX rates) and rising inflation rate.

In the Monetary Policy Committee meeting held on Monday 24th and Tuesday 25th May 2021, the MPC said the challenges facing the Nigerian Economy is stagflation as evident in the rising inflation and slow economic growth.

Still, the committee agreed that the strategies put in place by the central bank to rein in inflation through a series of administrative measures had started yielding results at 18.12 percent in April.

The nine-member committee also said the measures put in place to stimulate output growth through the use of its intervention facilities to inject liquidity into employment generating and output stimulating initiatives like the Anchor Borrower Program, Targeted Credit Facility and Agri-Business Small and Medium Enterprise Investment Scheme (AGSMEIS) had started to yield results.

However, the MPC said while the economy had exited the recession, the recovery remained fragile given that the GDP of 0.51 percent recorded in the first quarter of 2021 was far below Nigeria’s population growth rate.

The committee, therefore, agreed that there is a strong need for the Monetary Authorities to consolidate on all administrative measures taken to grow output. These measures should include consumption and investments, as well as diversifying the base of the economy through FX restrictions for the importation of goods and food products that can be produced locally in Nigeria.

“Whereas the Committee remained overwhelmingly committed to supporting the efforts of the Federal Government in ensuring full restoration of the productive capacity of the economy, members remained much more focused towards achieving price stability in the short to medium-term. The MPC noted that economic growth could be hampered in an environment of unstable prices,” the communique stated.

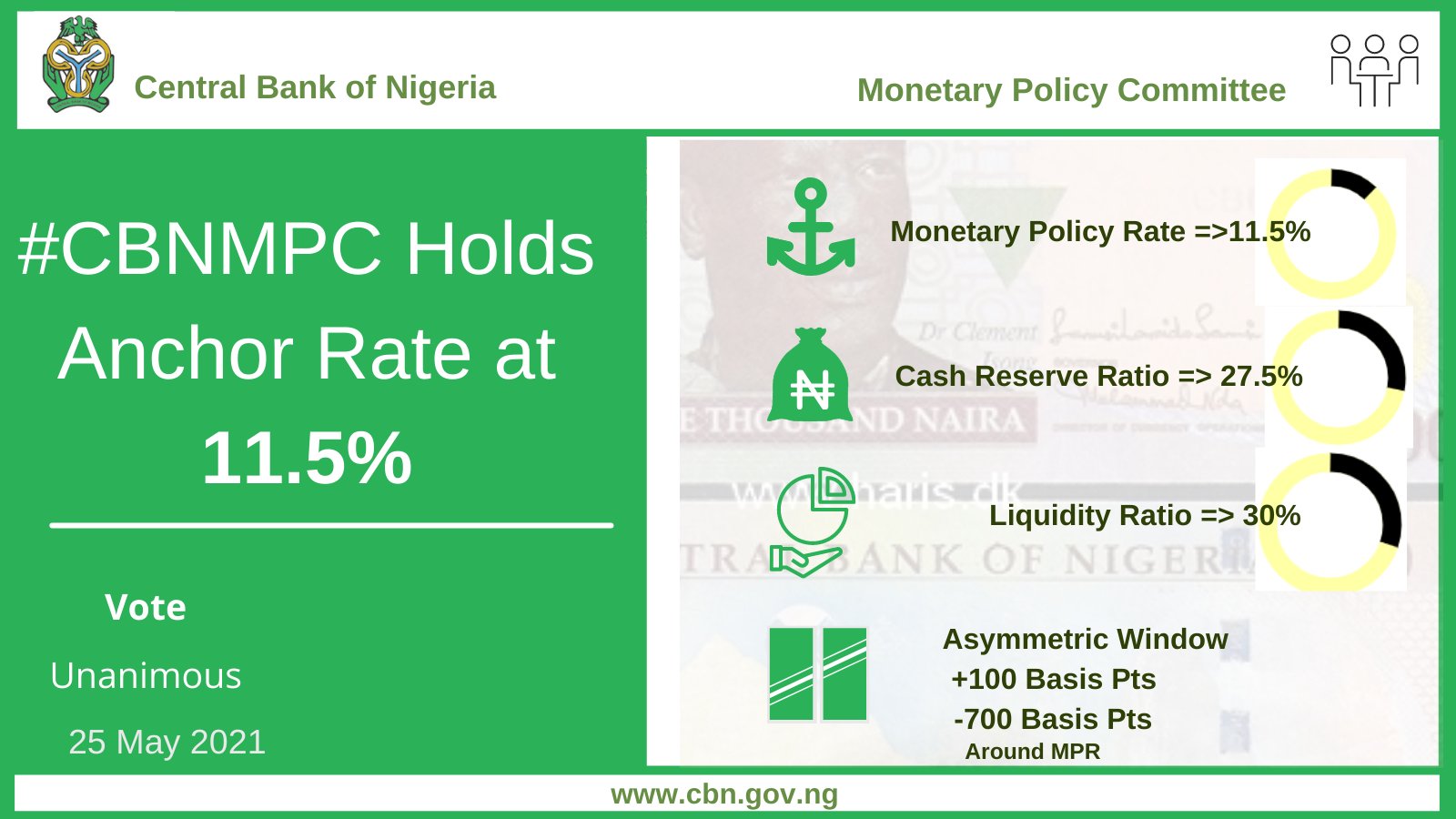

In spite of the aforementioned, the committee voted unanimously to leave:

- The Monetary Policy Rate (MPR) unchanged at 11.5 percent

- Retain the asymmetric corridor of +100/-700 basis points around the MPR

- Retain the CRR at 27.5 per cent

- Retain the Liquidity Ratio at 30 per cent.

The decision was because the committee agreed that an expansionary stance of policy could transmit to reduced pricing of the loan portfolios of Deposit Money Banks and result, therefore, in cheaper credit to the real sector of the economy. On the converse, this expected transmission may be constrained by persisting security challenges and infrastructural deficits.

“On the other hand, while a contractionary stance will only address the monetary component of price development, supply side constraints such as the security crisis and infrastructural deficits can only be addressed by policies outside the purview of the Central Bank. A tight stance in the view of members, will also hamper the Bank’s objectives of providing low cost credit to households, Micro Small and Medium Enterprises (MSMEs), Agriculture, and other output growth and employment stimulating sectors of the economy,” the committee stated.