Crude Oil

Crude Oil Rose Above $65 Per Barrel as US Production Drop Due to Texas Weather

Crude Oil Rose Above $65 Per Barrel as US Production Drop Due to Texas Weather

Oil prices rose to $65.47 per barrel on Thursday as crude oil production dropped in the US due to frigid Texas weather.

The unusual weather has left millions in the dark and forced oil producers to shut down production. According to reports, at least the winter blast has claimed 24 lives.

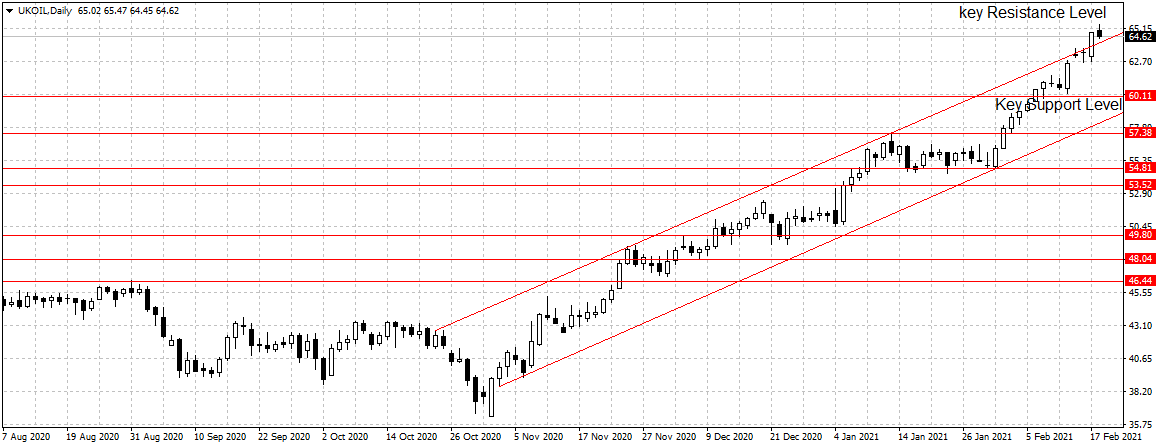

Brent crude oil gained $2 to $65.47 on Thursday morning before pulling back to $64.62 per barrel around 11:00 am Nigerian time.

U.S. West Texas Intermediate (WTI) crude rose 2.3 percent to settle at $61.74 per barrel.

“This has just sent us to the next level,” said Bob Yawger, director of energy futures at Mizuho in New York. “Crude oil WTI will probably max out somewhere pretty close to $65.65, refinery utilization rate will probably slide to somewhere around 76%,” Yawger said.

However, the report that Saudi Arabia plans to increase production in the coming months weighed on crude oil as it can be seen in the chart below.

Prince Abdulaziz bin Salman, Saudi Arabian Energy Minister, warned that it was too early to declare victory against the COVID-19 virus and that oil producers must remain “extremely cautious”.

Prince Abdulaziz bin Salman, Saudi Arabian Energy Minister, warned that it was too early to declare victory against the COVID-19 virus and that oil producers must remain “extremely cautious”.

“We are in a much better place than we were a year ago, but I must warn, once again, against complacency. The uncertainty is very high, and we have to be extremely cautious,” he told an energy industry event.