Markets

Market Outlook Jan 28 – Feb 1

- Market Outlook Jan 28 – Feb 1

This week will set the tone for the rest of the year as investors await Federal Reserve position on rate increase, Italy’s GDP to validate slowdown in Europe’s third-largest economy, Chinese Purchasing Managers Index to assess the level of global slow down, Australia’s inflation report to see if the improved unemployment rate and 21,600 jobs created pressured prices in December, BOJ monetary policy after lowering inflation projection for 2019 and the number of jobs created in the U.S in January following government shutdown.

The International Monetary Fund lowered its global growth projection for 2019 from 3.7 per cent to 3.5 percent last week, citing trade disputes and slowing growth in China after data showed the economy grew at a 28-year low in 2018. Signalling the effect of trade war on the world’s second-largest economy despite the People’s Bank of China’s stimulus to enhance productivity and sustain growth.

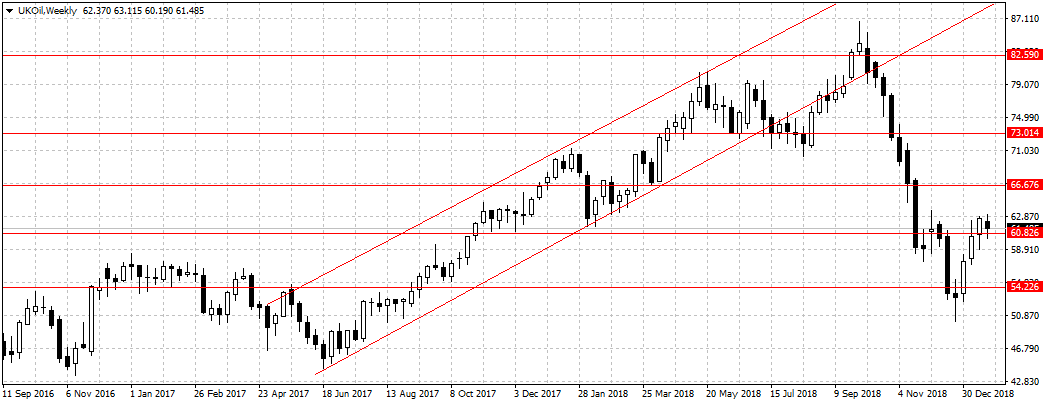

The weaker than expected growth stalled commodity prices – halted crude oil bullish move- as market confidence drop on possible slow down in oil demand. China is the world’s largest importer of crude oil.

Still, despite the increase in global risk, haven assets (currencies) failed to attract enough buyers to sustain 2018 growth momentum as investors fear risks could spread across the financial markets with the slowing growth in Euro-area, Brexit uncertainty, U.S shutdown and Fed wait and see approach.

In Euro-Area, the Bank of Italy cuts its 2019 growth projection for Italy from 1 percent to 0.6 percent, while the European Central Bank maintained current interest rates and warned on rising risks to growth.

“The risks surrounding the euro area growth outlook have moved to the downside on account of the persistence of uncertainties related to geopolitical factors and the threat of protectionism, vulnerabilities in emerging markets and financial market volatility,” Draghi said at a press conference.

The Euro currency dropped to a month-low against the U.S dollar after Mario Draghi, the ECB president, acknowledged that near-term data are likely to be weaker than expected. Further validating global perspective after a series of purchasing managers index showed growth in the region is slowing down. This week investors will look for more clues in the Italian economic report and ECB monetary policy to better assess the level of slowdown in the region.

Crude oil remained in a range ahead of U.S-China meeting this week, a positive outcome should boost oil outlook and support emerging assets. Still, the U.S. Fed’s monetary stance will determine capital inflow into the emerging markets.