Markets

Germany Services PMI Hits 7-year High

- Germany Services PMI Hits 7-year High

Germany’s services activity rose to a record high in January as surged in demand fueled business growth and job creation in the services sector.

The Services Purchasing Managers’ Index stood at 57.3 in January, up from 55.8 in December, according to the IHS Markit report released on Monday. The highest in nearly seven months.

Phil Smith, the Principal Economist at IHS Markit said: “With the final services numbers showing a slightly better outturn in January than that signaled by the earlier flash results, the overall rate of private sector output growth edged up since December to the strongest since April 2011.”

The survey also showed job creation rose higher, riding on 2017 momentum — the strongest economic growth in a decade. Meaning, the increase in business activity in the services sector aided job creation, with January seeing the highest job growth in nine months. While business backlogs rose for a 55 straight month in January.

Similarly, the report showed prices charged by businesses in Europe’s largest economy rose to the highest in almost a decade as the cost of business input grew in the month. Another indication of rising inflation and suggested that improved economic growth amid strong global growth will further pressure prices as suggested by the European Central Bank during the last monetary meeting. Businesses attributed the surged in price pressures to increase in oil and fuel prices, salary pressures and rising rental fees.

However, despite rising input costs, firms in the services sector were optimistic about economic growth in 2018. Business optimism was unchanged from what was obtained in December 2017.

“The survey results highlight the best round of job creation in the private sector economy for nearly seven years, which adds further pressure to an already-squeezed labour market. Panellists reported higher salaries contributing to sharply rising operating costs, the outcome of which was a pick-up in inflationary pressures. Prices charged for goods and services showed the steepest monthly increase since records began in late-2002,” said Philip.

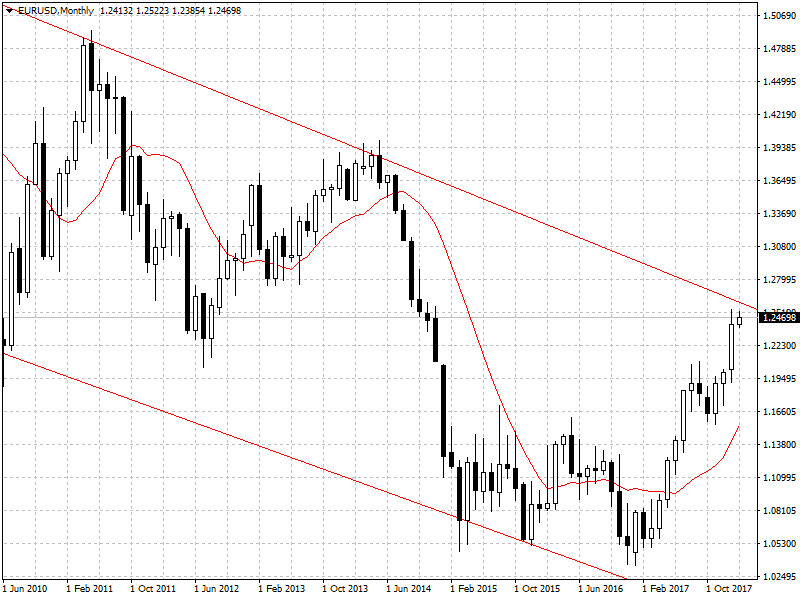

The Euro climbed from Friday low of $1.2409 against the U.S. dollar to $1.2468.

With the increased in price pressures and rising new job creation, the Euro common currency is likely to climb up to $1.2609 against the greenback, especially with the uncertainty in the U.S.