Forex

Forex Weekly Outlook October 17-21

- Forex Weekly Outlook October 17-21

The US dollar gained against most of its counterparts last week, despite the consumer confidence index (87.9) falling to a year low in September. The economy continued to create jobs by maintaining a four decade low unemployment benefits at 246,000 in the week ended Oct.8, same as previous week.

Also, consumer spending rebounded in September surging 0.6 percent from previously declining 0.2 percent in August, while the producer price index rose 0.3 percent for the first time in three months, indicating that consumer prices may be picking up as the increase in costs (energy and food) are pass-on to consumers.

This is one of the reasons consumer confidence dropped in the said month, as consumers are likely to react to increase in costs, and also it explained Fed’s position as to why aggressive steps “high-pressure economy” may be needed to lower unemployment further and boost consumption simultaneously, even if it means at a higher inflation rate.

Accordingly, the Fed Chair Yellen Janet during 60th annual economic conference in Boston, Massachusetts on Friday noted that extreme economic events like the world is currently experiencing have challenged existing economic views in terms of what drive growth (demand and supply).

While, admitting this will necessitate further research from the profession and the Fed, she said there were evidences from post-financial crisis that aggregate increase in demand lead to appreciable effect on aggregate supply against widely accepted notion that an economic output over the long-term is equal to its resources (labour, costs and existing technologies).

This was because at a more accommodative monetary policy (interest rate 0.5%), unemployment rate has remained nearly stagnant and so is the output. Therefore, throwing the possibility of a December rate hike in doubt, especially saying that the influence of the labour market, that the financial markets thought will force the Fed to hike rates to curb inflation above its 2 percent target, on inflation rate is weaker than had been commonly thought prior to the financial crisis. However, consumer prices report due on Tuesday and building permit of Wednesday will help assess the level of inflation so as to determine how close to target the Fed really is and economic growth.

In China, producer prices rose 0.1 percent for the first time in five years, bolstering consumer inflation to 1.9 percent in September. However, exports fell 10 percent from a year earlier, reducing the world second largest economy’s trade surplus to $42 billion, even with weaker Yuan. This suggested that weaker Yuan have little effect on exports as the global slowdown has impacted shipments from both the European Union and United Kingdom. For instance, exports to the EU has dropped 9.8 percent, while that of U.K. and U.S have declined by 10.8 percent and 8.1 percent respectively.

While the probability of exports turning positive is high due to continuous weakening of the Yuan by the Chinese central bank and the usual surge in Christmas orders, sustainability remains the question. Next week, third quarter GDP report, industrial production, fixed asset investment and National Bureau of Statistics (NBS) due on Wednesday will further throw light on the state of Chinese economy going forward.

In the UK, the sterling continued its decline against the US dollar and has so far lost 6 percent this month and down 17 percent this year. While Goldman Sachs and other analysts have said the embattled currency is still in for more punishment, the lower exchange rate will boost oversea orders and pressure consumer prices (inflation) above the Bank of England (BOE) 2 percent target.

This, will likely prompt BOE to either shun rising inflation and concentrate on growth as suggested by Mark Carney last statement on the economic outlook or attempt to curb inflation and risk growth. Inflation rate, producer prices, average earnings, consumer spending and unemployment rate are due this week, but these macro data are likely to have no positive effect on the economy as long as the confidence in the British market remains weak.

Overall, I expect the US dollar to lose some ground this week as investors look to understand Fed’s statement on the economy and come to terms with the possibility of the apex bank maintaining current interest rate while monitoring improvement across key sectors. This week I will be looking at CADJPY, USDCAD and EURNZD.

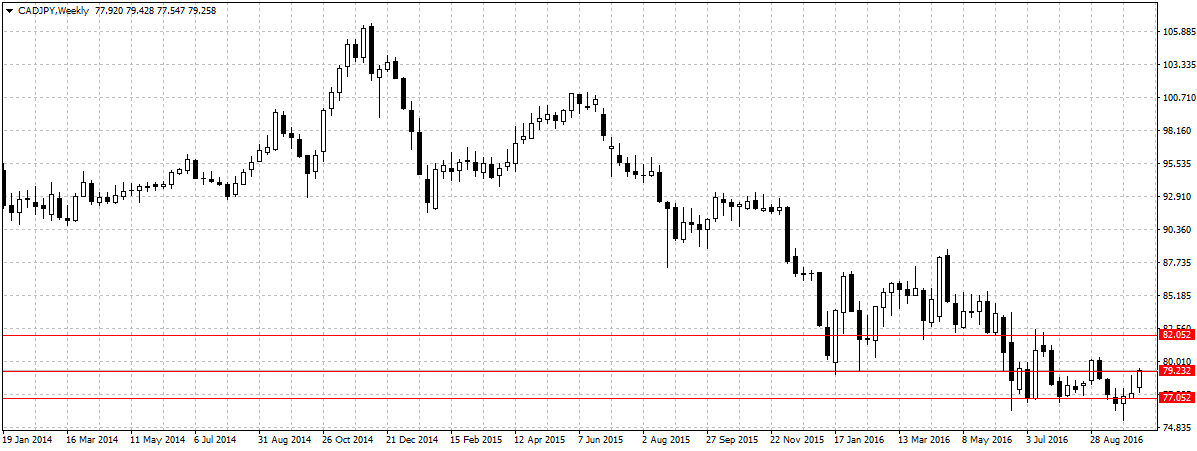

CADJPY

This pair plunged to four year low last month, largely due to the Yen continuous gain and low oil prices that weigh on oil-dependent loonie. But after OPEC members agreed to cut production in September the pair halted losses and has since gained 386 pips. Although, Canada economic data remain weak, there is a possibility that a rebound in oil prices will fuel an increase in investment and improve exports.

Click to enlarge

Technically, after a bullish pin bar was formed three weeks ago and the failure of the pair to break 77.05 support a week later showed this pair has halted the downward trend. But a sustained break of 79.23 resistance is needed to validate the bullish trend. This week, as long as price remains above 79.23, I am bullish on this pair this week with 82.05 as the target.

USDCAD

With the US dollar posed to retreat this week, coupled with the Russia and Saudi Wednesday’s agreement in Turkey to go ahead with production cut, this pair is expected to extend its decline this week. This week, I am bearish on this pair as long as 1.3142 holds with 1.3033 as the target.

Click to enlarge

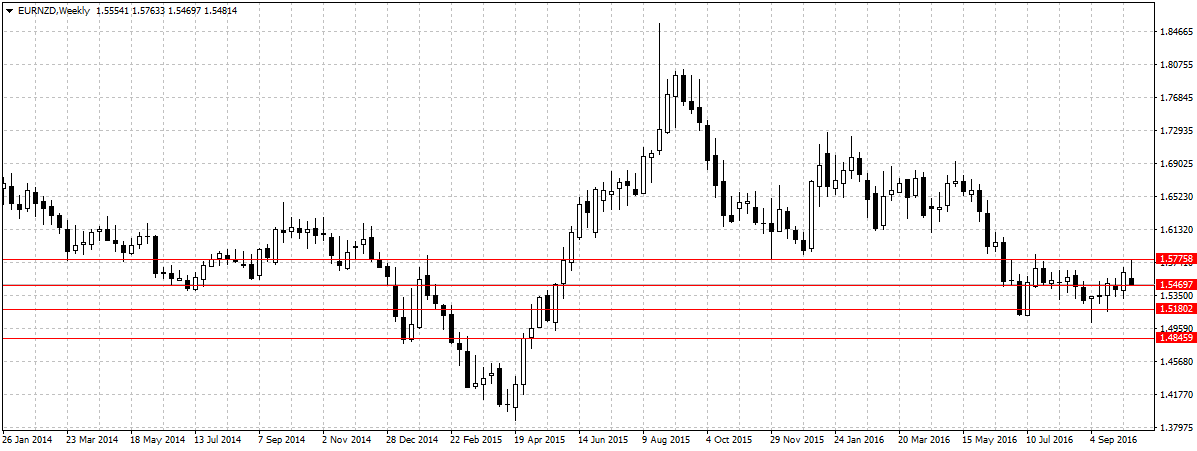

EURNZD

With the euro-single currency enmeshed in Greece debt and Brexit issues this pair will likely extend its decline this week – especially if last week bearish pin bar is taking into consideration. This week, as long as price remains below 1.5469 I am bearish on this pair this week with 1.5180 as the first target.

Click to enlarge

The EURUSD hit our first target at 1.1019 last week, but this week I will be standing aside on this pair to evaluate Euro-area economic situation in relation to how the financial markets react to the greenback after Fed’s speech.

AUDUSD touched our 0.7505 target and immediately lost most of its gains for the week. This week, I will be standing aside on Aussie to monitor market reaction to its current position for two reasons, one, the Aussie dollar does not have much room to grow on the bullish side considering its nearing 78.34 US cents, its one-year peak. Two, the US dollar is likely to give up part of its gains so far this week, and with buyers adding to their long positions without substantial data to explain the reason for Thursday and Friday attractiveness. I will be standing aside to better assess the situation.

NZDUSD

This pair was 44 pips short of hitting our target at 0.6989 last week, but this week I will be waiting for confirmation of trend continuity to sell per adventure Kiwi extend its decline against the greenback, but for now I will be standing aside also, while monitoring data from RBNZ and market reaction to the current position of this pair.