Economy

OPEC to Prop Up Oil Price by all Means

- OPEC to Prop Up Oil Price by all Means

Top producers in the Organisation of the Petroleum Exporting Countries (OPEC) are already looking at the possibility of extending production cut to prop up oil price if need be.

Iraq, Kuwait, and the United Arab Emirates representatives in the group agreed with Saudi Arabia that the cartel, along with its allies will extend the agreement for another six months per adventure price remained below an acceptable level. This may explain why Saudi Arabia set its 2019 oil benchmark at $80 a barrel.

Suhail Al Mazrouei, the energy minister, U.A.E, however, insisted that the 1.2 million barrel a day reduction agreed by the OPEC+ on December 7 will clear global supplies by the first half of 2019.

Mazrouei, who is also OPEC president, said in Kuwait that “the planned cuts have been carefully studied, but if it doesn’t work, we always have the option to hold an extraordinary OPEC meeting and we have done so in the past.”

“If we are required to extend for another six months, we will, if it requires more, we always discuss and come up with the right balance.”

Last week, oil price dropped to its lowest level in over a year despite OPEC cutting output, largely due to the projected slow down in global growth in 2019.

Experts believe slowing growth in China, Europe and the inverted yield curve will weigh on business confidence going into the new year and hurt global demands, especially with China been the largest oil importer.

Rising global trader wars, slow down in rates increase and the U.S. government shutdown are some of the key factors expected to impede growth and increase capital outflow from the world’s largest economy to the Euro-area and emerging economies with positive economic outlook in 2019.

Nigeria’s oil production is expected to be reduced by OPEC to 1.685 million barrels per day in the first half of 2019, down from its reference of 1.738 million bpd. Suggesting that foreign reserves of Africa’s largest economy is likely to drop even further in the first half of 2019 as the government expected to increase spending on capital projects in the first quarter to air campaign and sustain economic activities.

The nation’s foreign reserves declined from N47 billion in May 2018 to about N41 billion in November before rebounding slightly to N43 billion a week ago despite oil trading at $86 a barrel in September.

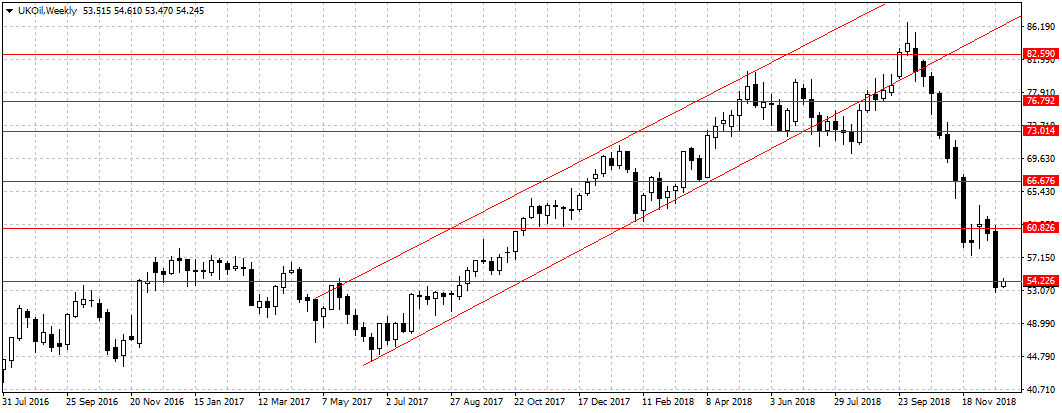

Price of Brent crude, against which Nigeria’s crude oil is measured, dropped to $52.8 a barrel on Friday.