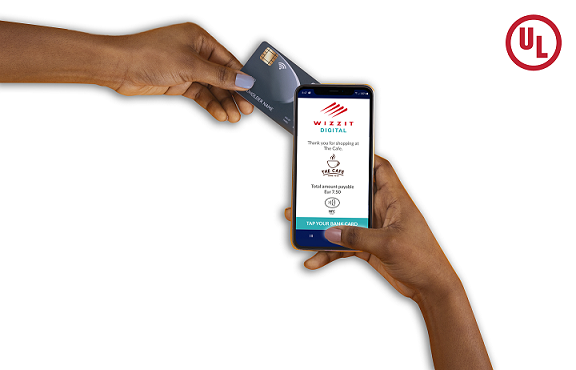

UL, the global safety science leader, has announced the completion of a pilot project with WIZZIT Digital to launch Tap2Pay SoftPOS solution with personal identification number (PIN) entry support.

This solution transforms commercial off-the-shelf (COTS) devices into point-of-sale (POS) payment terminals. Tap2Pay is the first SoftPOS solution developed in South Africa that supports PIN entry and is recognized by Visa and Mastercard. Since debuting the solution, WIZZIT Digital has gone live with an initial launch customer, one of the largest Pan-African commercial banks.

To navigate the complexities of bringing a SoftPOS solution to market, UL supported the Tap2Pay solution from development to marketplace entry. In the initial stages, UL provided advisory services to help WIZZIT Digital navigate the payments regulatory landscape and meet the payment schemes’ requirements. When Tap2Pay was ready for functional testing, UL tested it with a range of scheme-accredited tools to provide feedback on potential issues. Following debugging and troubleshooting, UL provided functional testing services and helped WIZZIT Digital gain Visa pilot type approval. After functional approval, UL’s security labs evaluated the solution for Mastercard’s and Visa’s security pilot programs. These tests and evaluations against scheme requirements allowed WIZZIT to bring the solution to market.

UL evaluation confirmed the Tap2Pay solution entered the marketplace, meeting key security requirements. This included ensuring the security of payment data obtained through a near-field communications (NFC) interface and a contactless kernel of the COTS device. The solution’s security mechanisms, controls and mitigations protect the consumer’s account data and other assets. The solution is compatible with a wide range of Android devices.

Explaining how Tap2Pay addresses an unmet market need, Brian Richardson, CEO and co-founder of WIZZIT Digital, said, “For almost two decades, we have been working with banks and financial institutions in emerging markets, including many countries in Africa. Our experience has taught us two things. Firstly, consumers and banks want the protection of a PIN when conducting contactless transactions. With cyberfraud on the rise, a PIN offers a universally accepted layer of security that people trust. Secondly, traditional cashless payment solutions are too expensive for micro and small merchants.

“For smaller merchants, the initial investment in terminals and the ongoing maintenance costs are simply too high. Tap2Pay SoftPos with PIN removes this barrier, enabling merchants of any size to accept cashless payments. This will ultimately help them attract more customers, including those who don’t want to pay cash for goods and services, for a fraction of the cost,” said Richardson.

Tap2Pay enters the market at a time when demand for contactless payment solutions is increasing. According to Deloitte, the COVID-19 pandemic has made the need for digitizing payments more critical than ever. However, many emerging markets are facing card acceptance challenges. For example, in South Africa, approximately 90% of the 100,000 nationwide shops in the informal sector only accept cash. To meet customer demand and increase card acceptance by the smaller business market, including merchants in rural areas, needs an affordable solution.

Jako Fritz, principal security adviser at UL, said, “SOFTPOS is an entirely new approach to digital payments lowering the barrier of entry for merchants to accept contactless card transactions. Cloud computing, as well as the Europay, MasterCard, and Visa protocol, allows the shift from traditional physically secure POS to software-based COTS transaction processing. These solutions will help micro and small business owners and merchants around the world meet the demands of an increasingly cashless society more securely with minimal investment.