Markets

U.K Wage Growth Picks Up Pace; Up 2.8%

- U.K Wage Growth Picks Up Pace; Up 2.8%

U.K wage growth picked up pace in the three months through January following consistent job creation, the Office for National Statistics said on Wednesday.

Wage growth excluding bonuses surged by 2.6 percent, and by 2.8 percent including bonuses when compared with a year ago. While the unemployment rate improved to 4.3 percent, the lowest since 1975.

This improvement in wage growth will support household spending and further boost retail sales now that the inflation rate has moderated from the record high of 3 percent to 2.7 percent in February. Meaning, retail sector may witness surge in both job creation and wage growth.

Also, the numbers highlighted the tightness of the labour market and point to recruitment challenges forcing businesses to up wages in order to attract and retain skilled employees. Therefore, the continuous job creation, expected further wage growth and the slowdown in consumer prices are expected to prompt the Bank of England to raise interest rates as early as May.

The total job creation between the month of November and January rose by 168,000 to 32.2 million, while unemployment number was boosted by the surge in the participation rate. Inactivity, people neither in work nor looking for a job, dropped by 136,000 during the period, the lowest in six years.

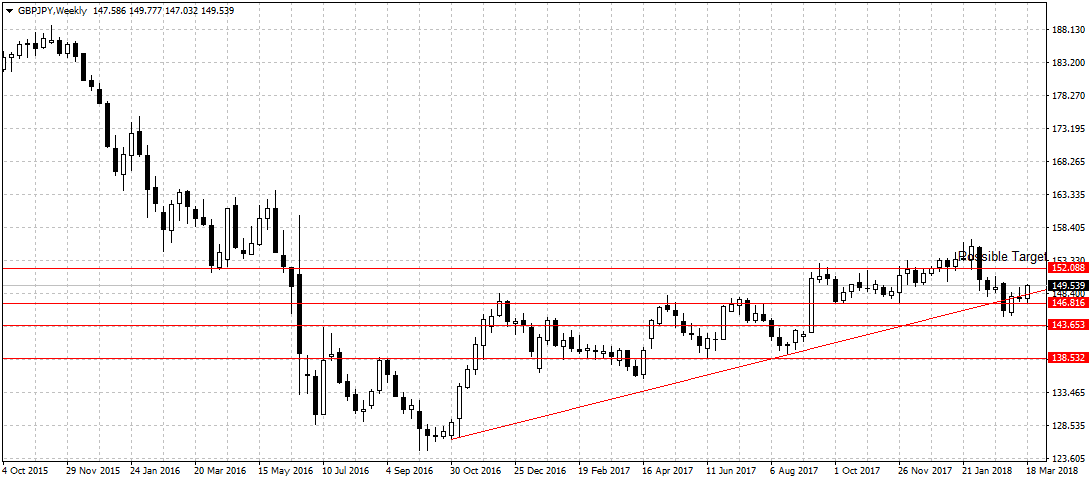

The pound rose 0.5 percent against the U.S. dollar to $1.4064 and additional 0.28 percent against the Japanese Yen after the report.

As stated here, we are bullish on the pound in the near term and expect the positive Brexit transition, strong economic data and expected rates hike to aid pound attractiveness.