Forex

Forex Weekly Outlook Jan 30 – Feb 3

- Forex Weekly Outlook Jan 30 – Feb 3

The US dollar was weighed upon by political uncertainty and weaker than expected GDP figure in the first week of the new administration. The economy grew by 1.9 percent in the final quarter of 2016, which was below the 2.1 percent forecast by analysts. The figures showed the US trade deficit widen as shipments of soybean that buoyed exports in the third quarter plunged, reducing net exports by 1.7 percent — the most since the second quarter of 2010.

But the continuous increase in household spending and surge in business-equipment spending for the first time in 5 quarters aided growth. While the value of all goods and services produced moderated to a 1.9 percent annualized rate, the economy remains strong, especially the industrial sector that saw Dow Jones closing above 20,000 points for the first time last week.

However, the uncertainty surrounding the series of changes being made by the new administration to existing policy has increased market volatility and risk exposure, making it hard to succinctly deduce market direction.

In the UK, the economy continued to differ Brexit doom and grew by 0.6 percent in the final quarter of 2016. More than the 0.5 percent forecast by economists. According to the report, manufacturing sector expanded 0.7 percent in the last quarter, bringing the 2016 total economic growth to 2 percent, down from 2.2 percent recorded a year ago. So far, the pound has lost 15 percent of its value since the June referendum and peaked at $1.2672 against the dollar on Thursday before closing at $1.2546.

In Australia, the consumer prices which measures inflation increased by 0.5 percent in the 4th quarter of 2016, which was below expectations of 0.7 percent. While on a yearly basis, inflation rate surged 1.5 percent, still below 1.6 percent predicted by analysts but up from 1.3 percent recorded in the previous quarter.

However, the Australian dollar continued to gain against the US dollar, despite the US dollar gaining against a basket of currencies. This is because investors are yet to make sense of Trump’s executive orders’ implications for both the US and global economies.

Overall, global uncertainty continued to weigh markets outlook amid changes in central banks’ policies. Therefore, it is imperative to pay attention to change in government policy and economic data from G-7 nations as they will form the bedrock of foreign exchange rate going forward.

Also, it should be noted that the U.K court has mandated Theresa May to entertain parliament vote on the final draft of the Brexit deal in March, this is a game changer as investors now have the opportunity to lobby for a better deal with the parliament. Hence, the surge in the pound.

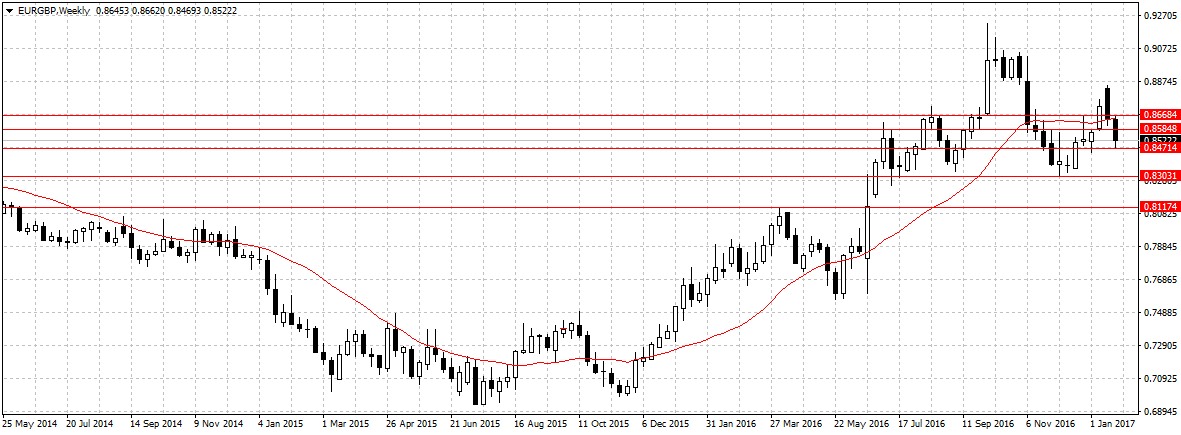

EURGBP

The Euro single currency economic outlook remained uncertain ahead of brexit, even though the manufacturing index shows business activities are beginning to pick up. The region is still struggling with a low inflation rate and weak oversea orders.

While the pound, on the other hand, remains vibrant as both the economic data and Prime Minister Theresa May’s efforts in rescuing the nation from post-brexit doom is gradually manifesting on the economy and projected to sustain investment sentiment in 2017.

Click to enlarge

This week, I will be looking to sell EURGBP below the 0.8471 resistance levels. This is because the bearish candlestick formed three weeks ago (1/15/2017) will be treated as lower high following the October 2nd, 2016 bullish candlestick that retraced about 40 percent to close at 0.9001 after peaking at 0.9224. The first target will be 0.8303, and 0.8117 will be the second target.

EURCAD

The Euro area is yet to rebound from its weak manufacturing sector and low consumer prices. While the Canadian economy is basking in the favourable US sentiment towards its exports and decision of the new administration to exempt the nation from 20% border tax owing to the fact that the US has a trade surplus of $11.9 billion with Canada in 2016, a relationship regarded by the administration as mutual beneficiary.

Click to enlarge

This positive sentiment will further support Canada positive economic outlook after OPEC production and boost its weak manufacturing sector in 2017. In lieu of this, I will be looking to sell this pair below 1.4070 price levels for our December’s target of 1.3742.