Forex

Forex Weekly Outlook December 5-9

- Forex Weekly Outlook December 5-9

The US economy continued its positive run last week, adding 178,000 jobs in November, and reducing its unemployment rate from 4.9 percent to a 9 year low of 4.6 percent. While the economy grew at a 3.2 percent annualize rate in the third quarter, more than the 2.9 percent initial estimations. The consumer confidence also surged to 107 from 100.8 in November, validating continuous job creation, even though wages dropped to -0.1 percent. The economy remains strong and in line with the Federal Reserve’s projection for interest rate hike in December.

However, the Organization of Petroleum Exporting Countries (OPEC) consensus on crude oil production cut last week, aided currencies of commodity dependent nations against the U.S dollar and bolstered emerging markets. This, first production cap agreement in 8 years is imperative to the financial market and expected to increase oil prices to about $55 a barrel in 2017 — provided non-OPEC members also agreed to production cap next week in Doha, Qatar.

In Canada, the economy expanded at an annualized rate of 3.5 percent in the third quarter and added 10,700 jobs at 6.8 percent unemployment rate. Boosted by the surge in crude oil prices, the Canadian dollar rebounded against the U.S dollar to close at 1.3282 last week and poised to continue this week as the financial markets price-in OPEC deal in relation to Canada economic progress.

In the UK, the manufacturing sector expanded by 53.4 in November, but below projected 54.4. The weak pound continued to impact production cost as manufacturers had to up prices charge for goods to accommodate surges in the cost of imported raw materials due to the difference in foreign exchange rate. Nevertheless, the Markit report showed companies from Europe, the Middle East and the US ordered more and projected to maintain current level going forward. This combined with Brexit Secretary David Davis assertion that the U.K would secure access to the EU single market post-Brexit, bolstered pound to a two-month high against the U.S dollar last week. Again, this is another indication of how vulnerable the pound will be in a series of comments from policy makers as the U.K prepared to trigger article 50 in March, 2017.

Therefore, traders are advised to pay attention to changes in economic policies as the U.S, U.K, Italy, France, Japan etc. adjusts their policies to better accommodate present market reality. Meanwhile, this week NZDCAD and EURGBP top my list.

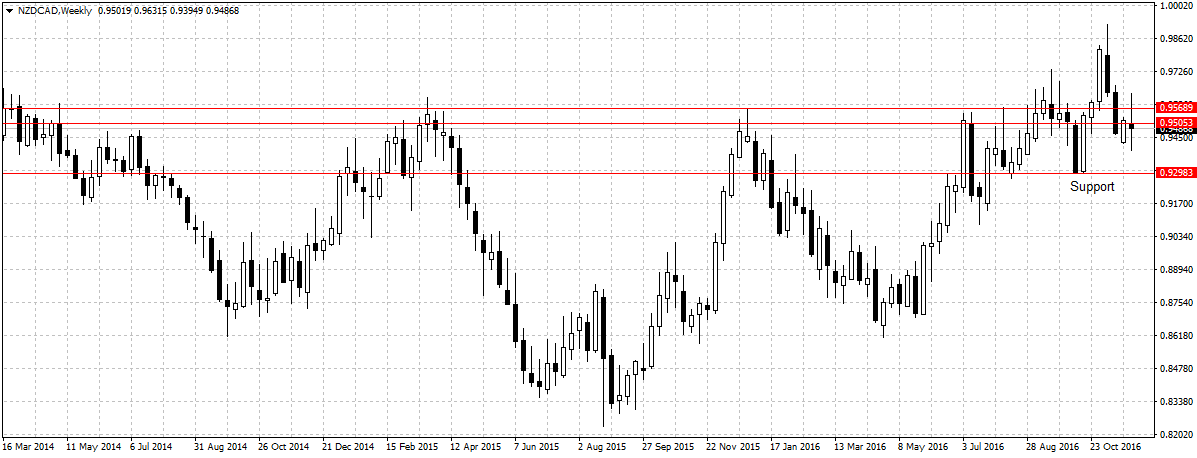

NZDCAD

This commodity dependent pair stand-out for several reasons, one, Canadian currency/economy has picked up after Alberta’s wildfire, and projected to do better as OPEC and non-OPEC strive to reach consensus on production cut. Two, all through this year I have emphasized why the Kiwi is overpriced and the reason it will eventually pared gains, and aligned with the reserve bank of New Zealand foreign exchange rate projection. While, emerging economies are expected to get a boost from the surged in commodity prices and rebound in the manufacturing sector, Canada is at the heart of it all and forecast to do even more, especially with Trump plans to increase productivity in the U.S — Canada largest trading partner, the Canadian manufacturing sector is expected to once again come alive and continue to support job growth and income, which will eventually encourage consumer spending and spur inflation from the current low.

Click to enlarge

Technically, this pair has lost about 529 pips, after peaking at 0.9923 three weeks ago — closing as doji below 0.9505 psychologically level last week. This week, I am bearish on NZDCAD as long as 0.9505 new resistance holds, with 0.9298 as the target.

EURGBP

This pair topped our list last week and since then has lost about 101 pips in our favour to close bearish at 0.8373, this week I remain bearish on EURGBP, one, the Italy referendum, France election, Greece economic issues, among other Europe economic struggle are likely to weigh more on the Euro single currency against the British pound this week. Another reason is the current pound position, the U.K economy/currency continued to differ post-Brexit catastrophe and pared losses.

Click to enlarge

This week, as long as 0.8471 holds, I am bearish on EURGBP, with 0.8240 as first target and 0.8117 as the second target.

This two pair remains elusive, even with the US dollar renewed strength ahead of the Fed’s rate decision, these commodities dependent currencies remain moderately attractive and has managed to remain above comfortable sellers-price level in the last two weeks. While I remain bearish on both pairs. I will be standing aside this week to better monitor these economies in relation to a series of global happenings impacting these pairs.