- Forex Weekly Outlook November 7-11

The US dollar continued to drop ahead of the US presidential election, even with a “positive” payroll report, the currency dip further. The labor market added 161,000 jobs in October, below the 174,000 expected by economists, but strong enough to validate Fed’s rate hike decision come December. This is because, the surge in wages to 2.8 percent (year-on-year) confirmed the optimum of the job market and the struggle to keep employees as employers compete for limited skilled-workers.

Also, the unemployment rate improved to 4.9 percent in October, despite the fact that the 12.1 percent of the “unemployed age group” voluntarily quit their jobs with the confidence of securing a high paying job. While, the participation rate that contributed to the 5 percent unemployment rate recorded in September declined, boosting the outlook of the job market.

However, there are discrepancies in the recent data that could change Fed’s growth approach and sustenance. For instance, productivity in the services sector fell to 54.8 in October from 57.1 percent in September, while business activity plunged to 57.7 in the same month. Even though, it still reflects expansion, stalling growth may begin to worry policy makers and prompt them to adopt what Fed Chair Yellen Janet called a “high pressure economy” during her last month speech — by going above her target for both employment and inflation in order to attract more investment and hiring to lower unemployment even further.

Nevertheless, the November 8 presidential election could change the entire global economic outlook and compel investors and businesses to adopt new growth model as they strive to comprehend the new government policy from the world largest economy. This week, high volatility is expected across board, but a Clinton presidency should stabilize the markets and reinforce the likelihood of the Fed’s raising rates in December and vice versa.

In the UK, the pound climbed on Thursday following the Bank of England (BoE) decision to leave interest rate unchanged at 0.25 percent, and a court ruling stopping the Prime Minister Theresa May from triggering article 50 of the Britain’s exit from the European Union without the U.K. parliamentary approval. While, the pound might extend its gains in the coming days as investors scramble to cover their short positions, the downward pressure is likely to persist due to economic uncertainty surrounding Brexit.

Accordingly, depreciation of the pound is expected to boost exports and reduce imports as UK products become affordable for overseas buyers and Britons choose to purchase locally made products, rather than expensive imported alternatives. Therefore, trade balance deficit is expected to exceed current level by 2017.

While, the U.K. fundamental point to growing economy with solid manufacturing sector (54.3), resilience services sector (54.5) and economic growth rate of 0.5 percent in the third quarter, the unexpected progress post-Brexit could be affected by the uncertainty in the UK economic outlook, and worsen if the country had hard-Brexit – ‘leaving the European Union without access to the single largest market of approximately 500 million consumers.’

“This is because EU deals are the biggest determinant of the UK economic outlook going forward.”

In Japan, the Bank of Japan held its annual 80 trillion yen ($764 billion) bond-buying program unchanged, while delaying the timing for reaching its 2 percent inflation target. Despite, inflation falling 0.5 percent in September — for a seven straight month and consumer spending declining 1.9 percent, the apex bank remained resolute in its current monetary policy (controlling short- and long-term rates and its asset-purchase programs).

According to the Bank of Japan Governor, Haruhiko Kuroda, the institution didn’t take additional monetary measures because the outcome of the US election will not just affect the U.S. economy but would have important implications on global economy, hence, the apex bank is keenly monitoring the outcome in relation to the global economic reaction to these developments.

In lieu of global developments ahead of US presidential election this week, the yen, will continue its gains against the US dollar and other perceived high-risk currencies as investors increase their holdings of haven assets in an effort to avert Brexit similar occurrence. This week, AUDJPY and USDJPY top my list.

AUDJPY

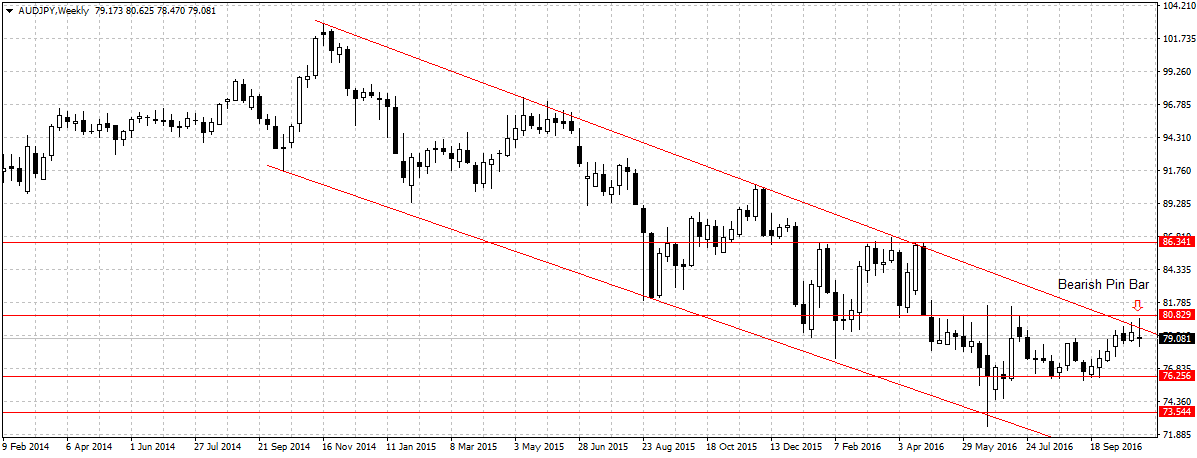

On July 4th, I mentioned the significance of AUDJPY descending channel here, ever since, this pair has traded within the channel. Last week, AUDJPY failed to sustain its gains above 80.82 resistance, closing once again below the established channel as a bearish pin bar — this further validated the significance of the descending channel to the economic outlook of the pair.

Another reason why this pair holds potential, is the increasing global uncertainty and risk ahead of the U.S. presidential election. Naturally, investors are risk averse, and gravitated towards haven assets to avert possible loss in case there is disparity in the outcome of the election and market expectation. In this case, the yen is a better haven asset and likely to attract more buyers this week.

This week, I am bearish on the AUDJPY as long as price remains below 80.82 resistance, I will be looking to sell below last week close of 79.08 for 76.25 as the target.

USDJPY

Last week, the US dollar lost 249 pips against the yen to close at 103.03, the lowest in a month. While, the US economy is vibrant, the uncertainty surrounding the election continued to weigh on the currency and has plunged it against all the majors. This week, I am bearish on USDJPY, one, because of the possibility of the pair to drop further as investors increase their holding of Japanese yen, while assessing the U.S. election result.

This week, I will be looking to sell around 102.68, below 20-day moving averages, while targeting 101.47 first, with 100 as the second target. But a Clinton presidency will void this analysis and solidify the US bullish run.

{kind=link}

{kind=link}